Learning Resources

Latest Stories

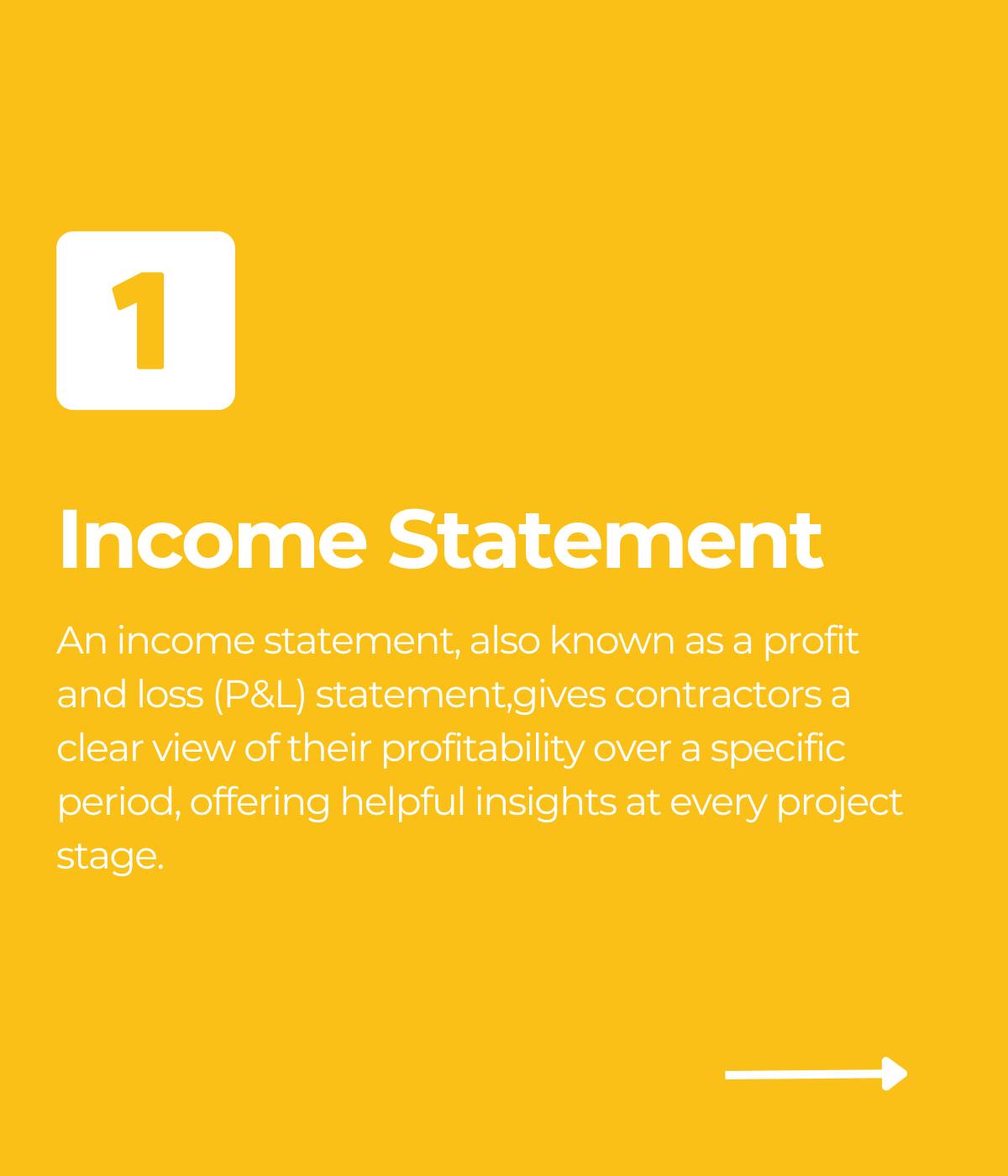

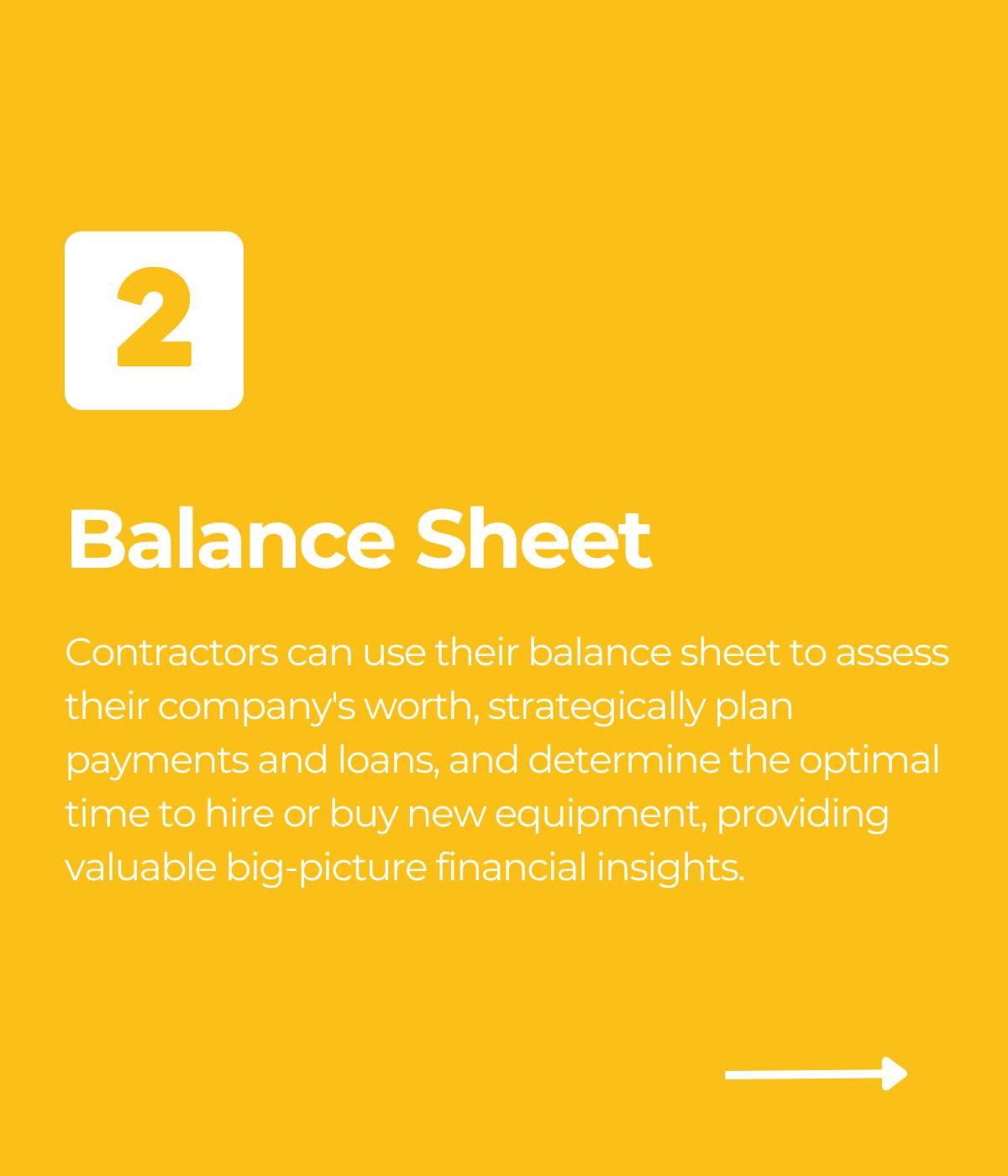

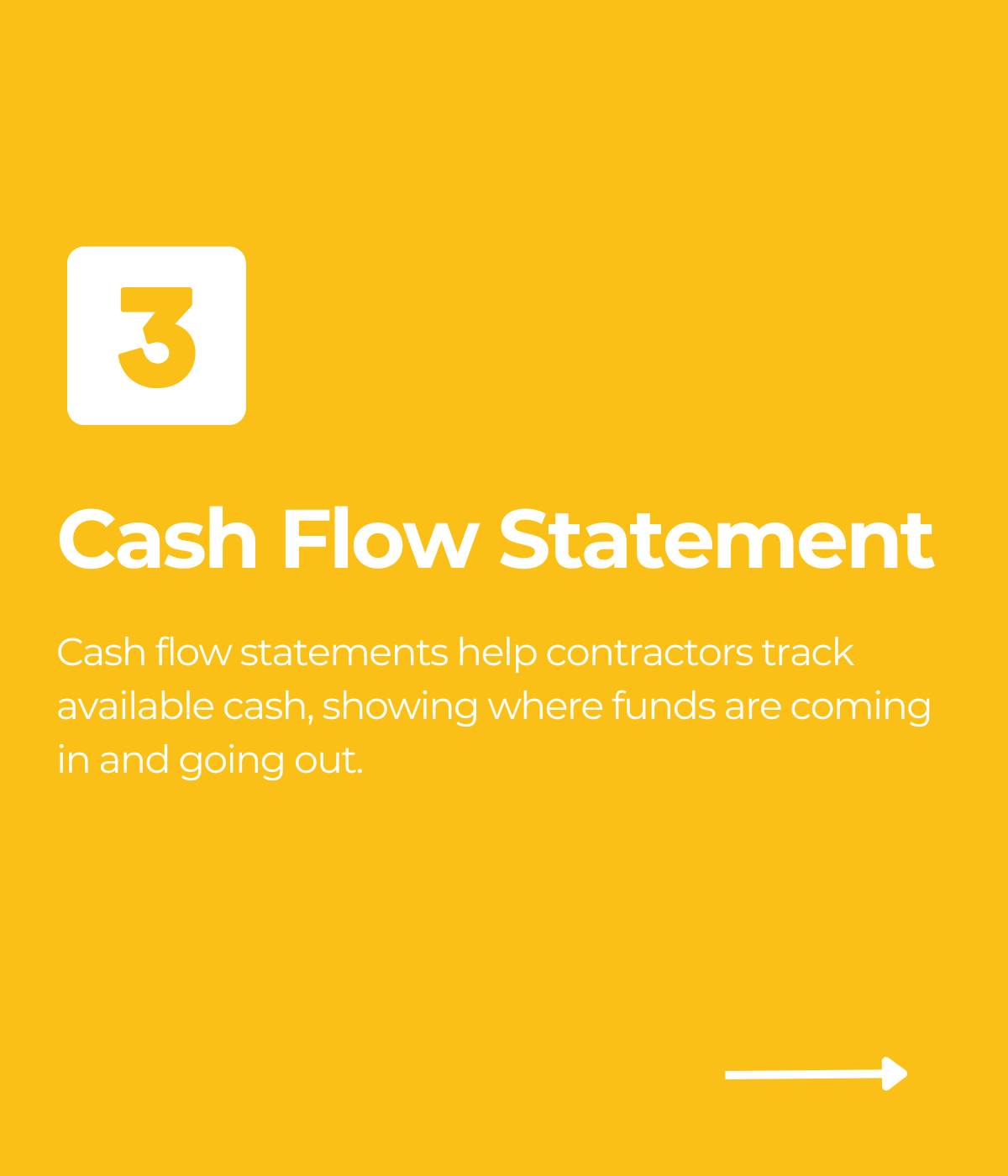

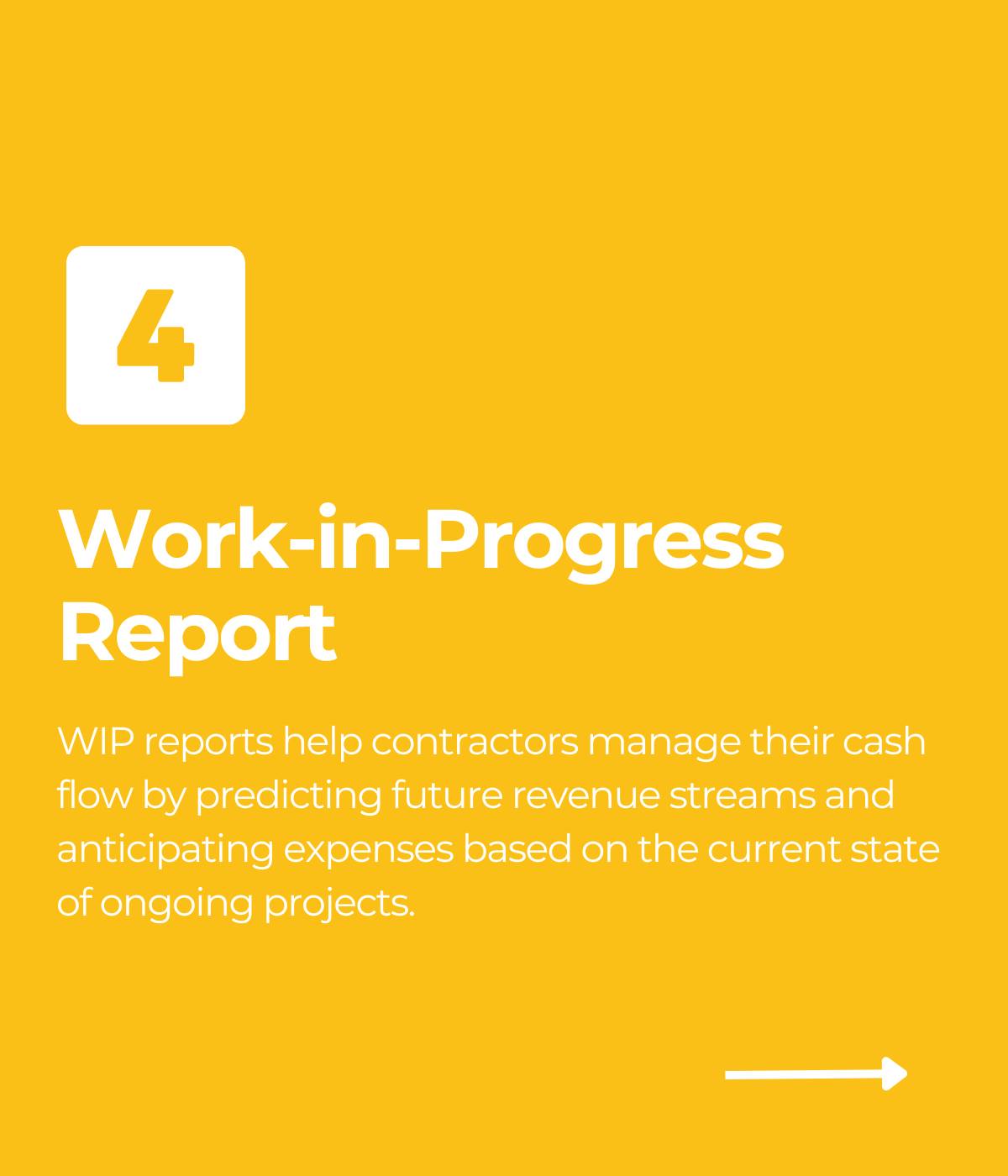

Why a Construction CPA Can Be a Contractor’s Best Friend

Managing finances for a construction company comes with its unique set of challenges. From tracking project costs and managing cash flow to

Learn More

Deep Dive Into Construction Project Phases

Construction projects are becoming increasingly complex, requiring contractors to rely on construction project phases to break down the entire job

Learn More

Construction Company Grows To $15M In Revenue Using Foundation® Accounting Software

Construction Company Grows To $15M In Revenue Using Foundation® Accounting Software

Learn More

Evaluating the Current State of Labor in Construction

A lot of my recent conversations with industry professionals have revolved around labor concerns. The economic headwinds caused by tariffs

Learn More

Why Technology Matters for Construction Job Costing

Construction job costing helps contractors track their spending to keep their projects within budget and maximize their profits. Traditional manual

Learn More

Want to See More Stories Like These?

View more educational resources to build your business and improve your processes.

View More

Make Your Inbox Smarter

Stay up to date with current news & events in the construction industry. Subscribe to free eNews!Our Top 3 YouTube Videos

Learn about our software more in depth with product overviews, demos, and much more!

ACA & W-2 Services

Our ACA reporting & e-filing services include official 1094-C and 1095-C IRS reporting, optional e-filing (no applying for a TCC code required), mailing to your employees and experienced support to help you.

Client Testimonials

There are plenty of reasons to make FOUNDATION your choice for job cost accounting and construction management software — just ask our clients!

Product Overviews

From job cost accounting software, to construction-specific payroll. Get an overview on your next all-in-one back-office solution.

Recommended Reading

Educational resources to help build your skills and business.