Read Time: Less than 4 Mins

First Published: October 16, 2020

Signed into law on December 2017, the Tax Cuts and Jobs Act — or TCJA, as it’s commonly abbreviated — represents the biggest overhaul of the US tax code in recent history. While the TCJA introduced new guidelines to deductions typically claimed through Section 179, it also provides business owners with additional options for claiming bonus depreciation on qualifying purchases — including deductions on new software purchases for their businesses.

As a result, business owners now have more options than ever when it comes to claiming deductions on purchases for their businesses. But to do so effectively, it’s necessary to understand the differences between Section 179 and bonus depreciation under the TCJA.

What’s the difference between Section 179 and bonus depreciation through the TCJA?

Section 179

Bonus Depreciation

Deductions for Software

Yes. New software purchases qualify.

Yes. New software purchases qualify.

Deduction Limits

Yes. $1.22 million within a single year, with yearly increases to compensate for inflation.

No. No limits on deduction claims.

Claim Limited to Income

Yes. Deduction claims are limited to less than annual income.

No. Deduction claims aren’t limited by annual income.

Real Estate Improvements

Yes. Can be claimed for improvements to property.

No. Improvements to real estate are not covered.

Split Claims Over Time

Yes. Claims can be partially split so some deductions can be taken now and others can be expensed in later years.

No. All bonus depreciation must be claimed in the tax year when the purchase was made.

Expiring Returns

No. New deductions can be claimed yearly with the same stipulations.

Yes. 100% bonus depreciation is only available until 2022. Starting in 2023, 20% decreases occur yearly.

Section 179:

- Carries a maximum deduction limit of $1.22 million per year. If you spend more than this in a year, your deductions decrease.

- Deductions are limited to less than your annual business income.

- Claims are flexible. You can split deductions individually, so 50% of the cost of new purchases can be deducted now while the rest is deducted over time.

- Real estate upgrades up to $3.05 million qualify. Upgrades to currently owned property can be included in a Section 179 deduction, unlike with bonus depreciation.

TCJA Bonus Depreciation:

- No deduction limits. Even if you spend over $1.22 million on qualified purchases in a tax year, you can still claim the full deduction.

- Deduction can be larger than your annual business income.

- Less flexibility in claims. Any deductions must apply to 100% of asset costs within the same category. If 100% bonus depreciation is taken on a qualified three-year asset, all three-year assets purchased within the same year must also be claimed through bonus depreciation.

- Time is limited. 100% bonus depreciation is only available through 2022. Starting in 2023, deductions are decreased by 20% until it phases out completely in 2027.

Getting the Most out of Your Deductions

To get the most out of their deductions, owners can even use a combination of Section 179 and bonus depreciation. Owners should discuss their options with their CPA, particularly one focused on the construction industry. If you don’t regularly work with a CPA, check out our CPA directory to find one in your area so you can discuss how to maximize your tax benefits this year.

Share Article

Make Your Inbox Smarter

Keep on current news in the construction industry. Subscribe to free eNews!

Related Articles

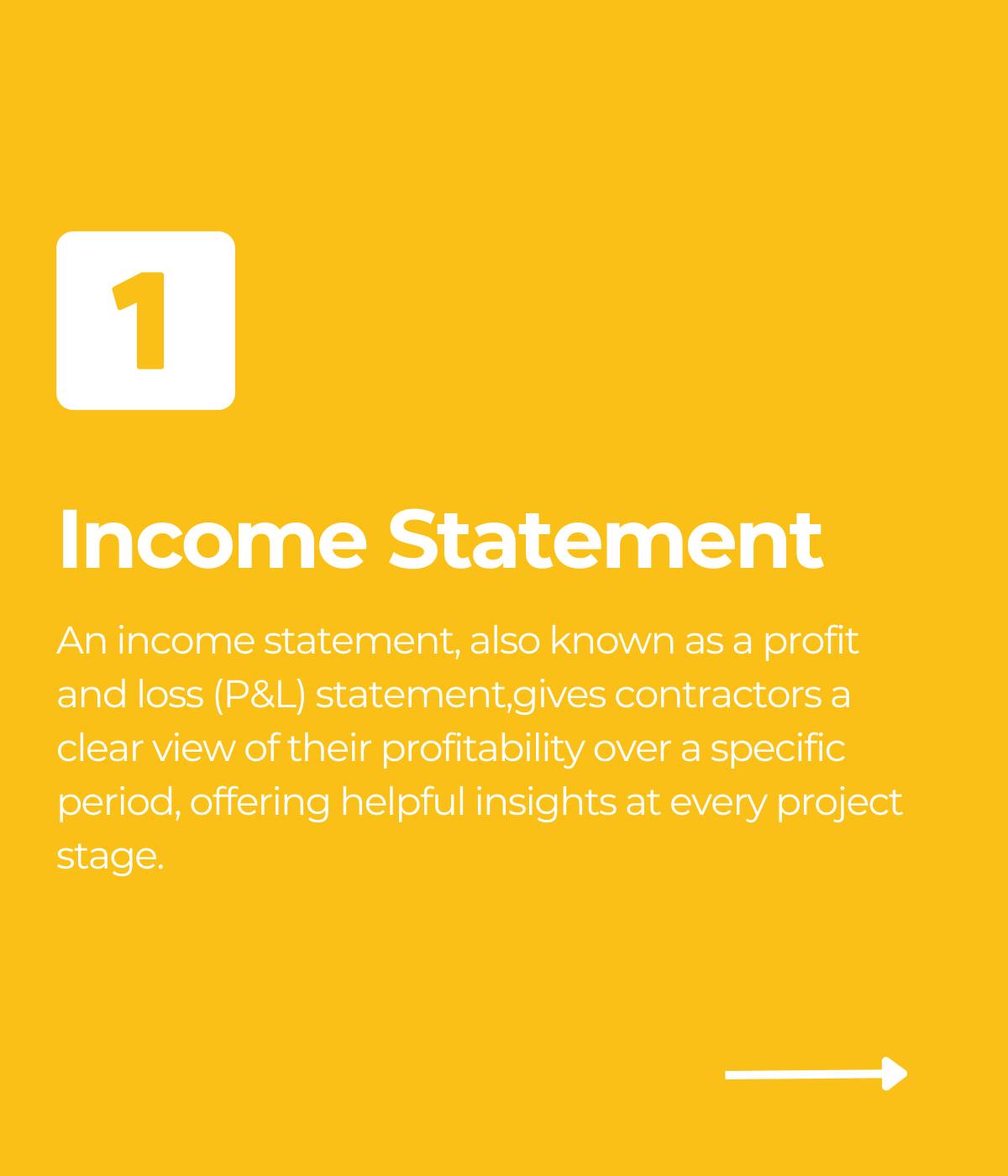

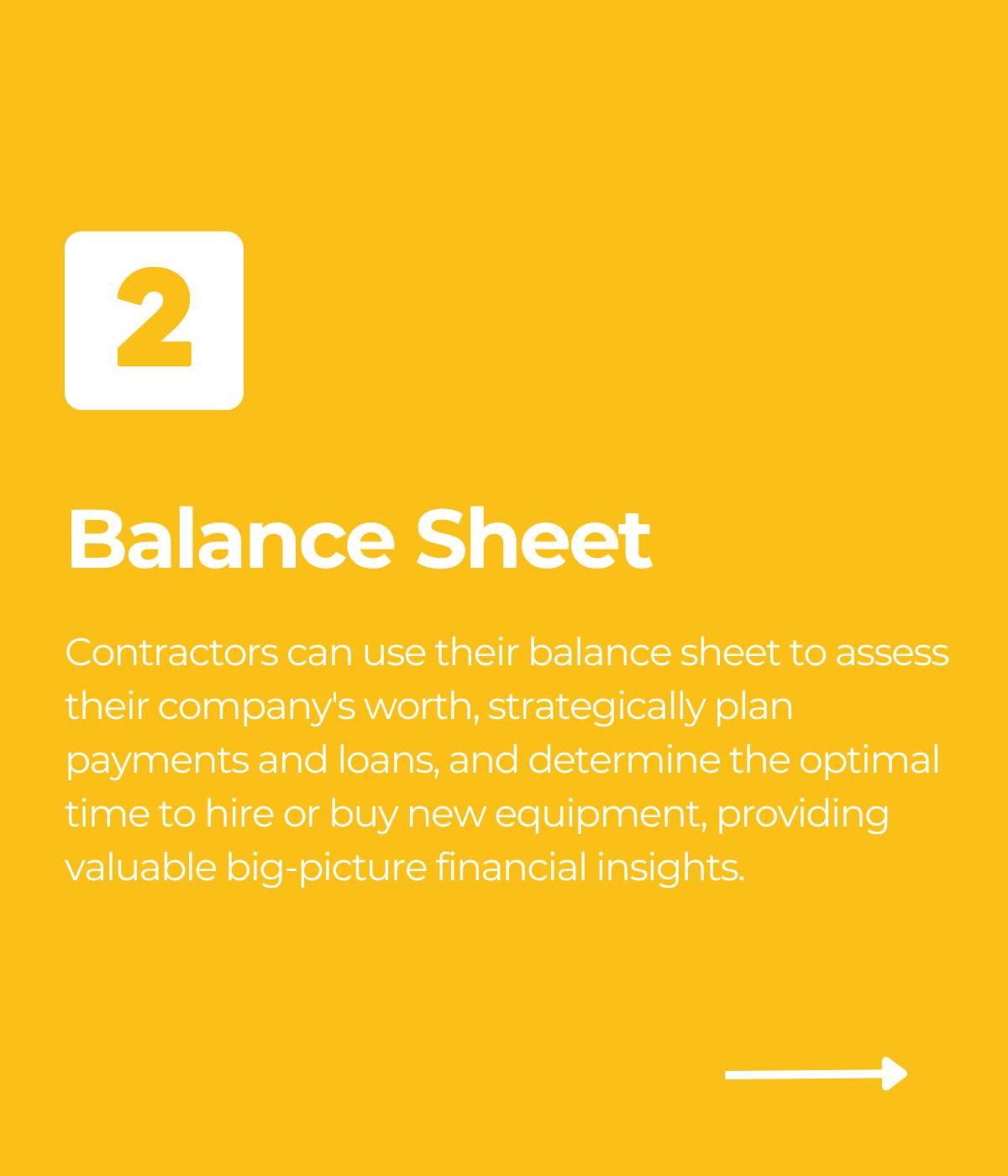

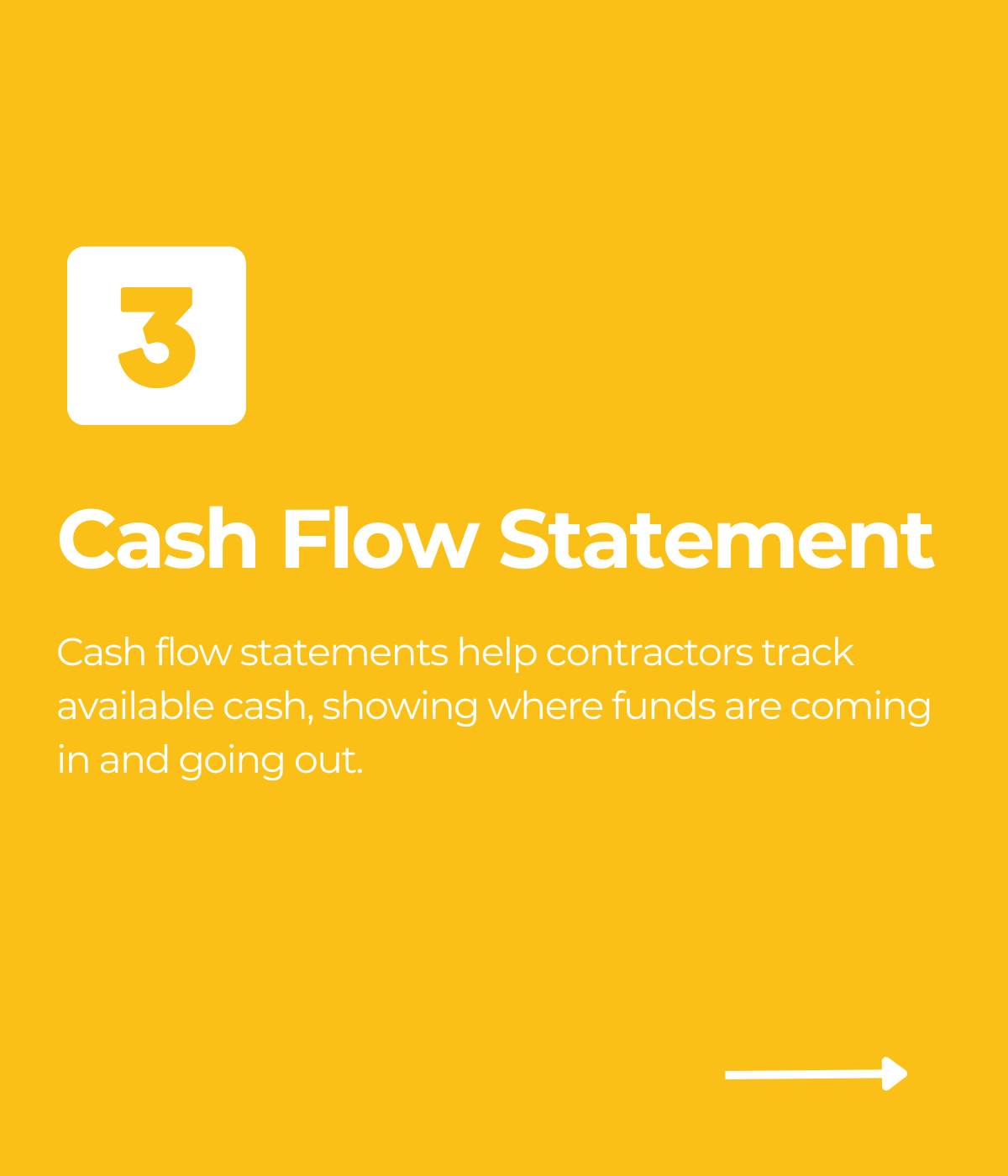

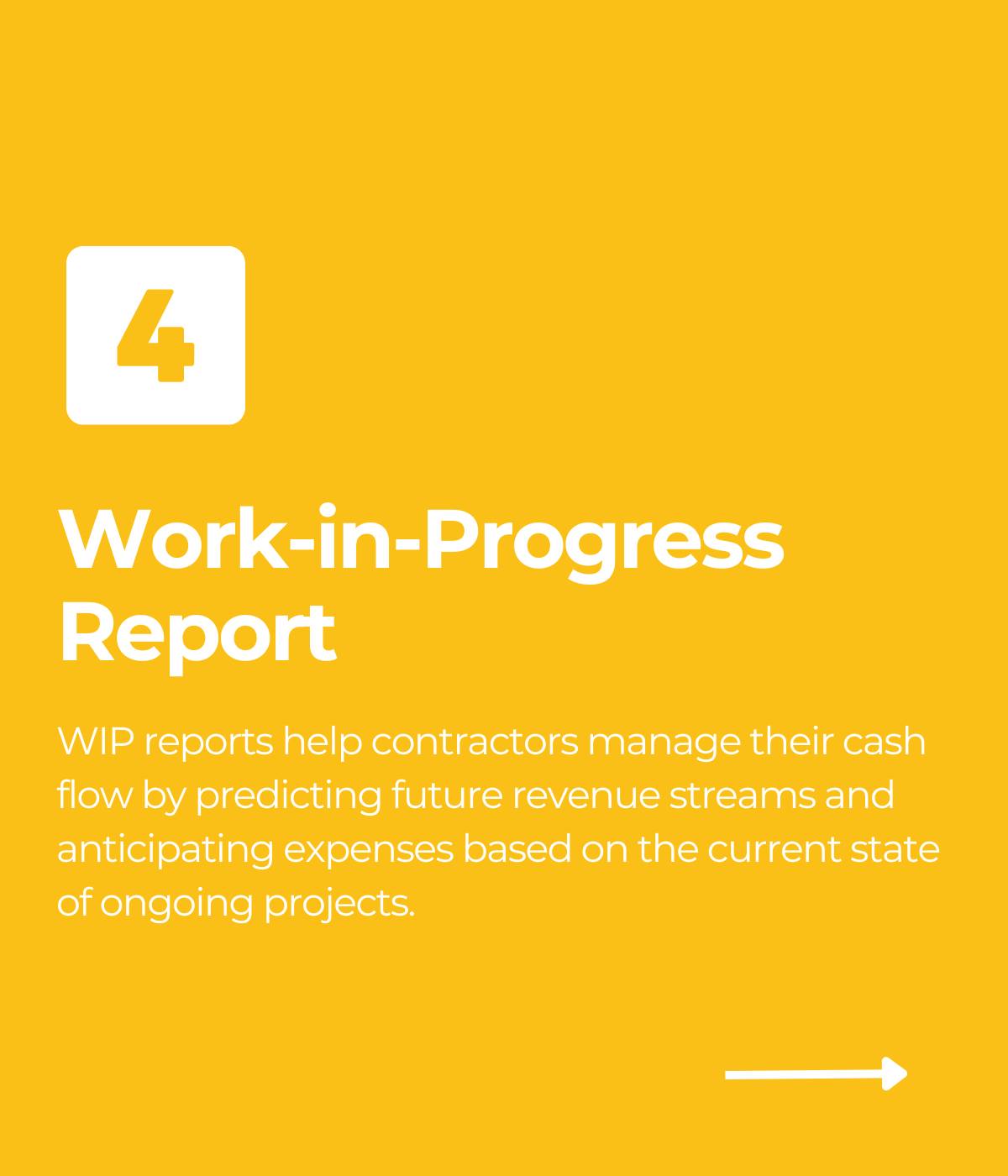

Top 5 Construction Reports and How They Help Your Business

Construction reports are the financial backbone of a contractor’s business. Contractors leverage these reports to make decisions that are critical

Learn More

How to Select Construction Accounting Software for Your Company

Before selecting a construction accounting solution for your company, it’s important to research your choices and evaluate your company’s needs.

Learn More

Our Top 3 YouTube Videos

Learn about our software more in depth with product overviews, demos, and much more!

ACA & W-2 Services

Our ACA reporting & e-filing services include official 1094-C and 1095-C IRS reporting, optional e-filing (no applying for a TCC code required), mailing to your employees and experienced support to help you.

Client Testimonials

There are plenty of reasons to make FOUNDATION your choice for job cost accounting and construction management software — just ask our clients!

Product Overviews

From job cost accounting software, to construction-specific payroll. Get an overview on your next all-in-one back-office solution.